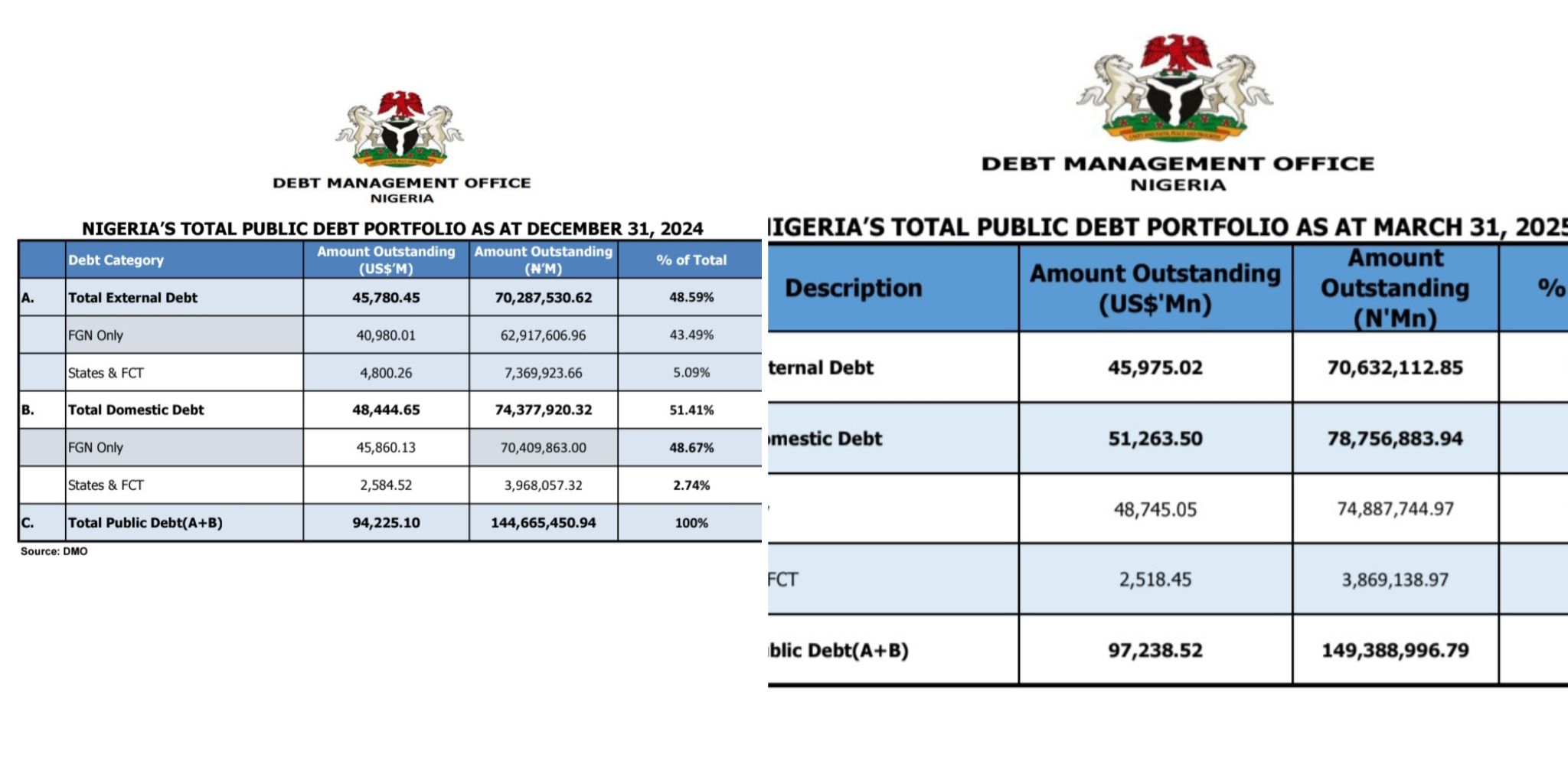

Nigeria’s public debt has once again climbed, reaching a staggering ₦149.3 trillion as of March 31, 2025, according to fresh figures reviewed from the Debt Management Office (DMO). This marks a sharp rise from ₦144.6 trillion recorded just three months earlier, in December 2024.

The breakdown of the data shows the bulk of the increase came from domestic borrowing, which jumped by ₦4.4 trillion—from ₦74.3 trillion to ₦78.7 trillion between December and March. External debt also edged upward by about ₦350 billion, moving from ₦70.28 trillion to ₦70.63 trillion within the same period.

This upward trend isn’t new. Nigeria’s total debt has been climbing quarter after quarter. By September 2024, the total stood at ₦142 trillion, up from ₦134.2 trillion in June. Back then, external debt was at ₦63 trillion, while domestic debt was ₦71.2 trillion—out of which the federal government alone was responsible for ₦66.9 trillion, and state governments accounted for ₦4.2 trillion.

By December 2024, the situation had worsened. The country’s debt crossed ₦144 trillion, with external loans hitting ₦70.28 trillion and domestic debt rising to ₦74.3 trillion.

Despite the federal government’s repeated assurances to rein in borrowing, the numbers tell a different story. In August 2023, President Bola Tinubu had publicly promised to end what he called the “vicious cycle” of excessive borrowing. At the inauguration of the Presidential Committee on Tax Reforms, he stated his firm intention to cut back on loans and reduce the burden of debt servicing on Nigeria’s limited revenues.

The official State House release from that event quoted Tinubu saying:

“President Bola Tinubu in Abuja expressed his resolute commitment to break the vicious cycle of overreliance on borrowing for public spending, and the resulting burden of debt servicing it places on the management of Nigeria’s limited government revenues.”

However, the steady rise in debt paints a picture of a country still deeply reliant on loans to fund its operations. Even as the Tinubu administration touts tax reforms and revenue diversification, Nigeria continues to lean heavily on domestic lenders, with local debt making up the bulk of the portfolio.

Analysts say without a radical shift in fiscal discipline and a clear strategy for revenue expansion, Nigeria’s rising debt load could put pressure on future budgets, raise debt-servicing costs, and hinder critical development projects.

For now, the trend continues upward—with no sign of slowing.